Gen Z Guide: How to Build a “Mortgage-Ready” FICO Score from Scratch

So, you're ready to level up and start thinking about homeownership someday. Maybe not today, but one day soon. The best part? You can start preparing right now — even if you’ve never borrowed money before. It all starts with your FICO Score — that magic number mortgage lenders use to decide if you’re financially trustworthy. Let’s break down how to build your credit the smart way, with your future home in mind.

7/8/20252 min read

What Makes Up Your FICO Score?

Your credit score is a numerical representation of your statistical likelihood to repay credit that is extended to you. Mortgage Scores range from 300-850. Your score is a “snapshot” of a specific moment and can change with new actions and the passage of time.

FICO Scores are calculated from different data that can be grouped into five categories as outlined below. The percentages in the chart reflect how important each of the categories is in determining your FICO score.

Your Credit-Building Blueprint

1. Start With One Credit Card (If You Haven’t Already)

If you’re starting from zero, try:

Capital One or Discover

Or a secured credit card such OpenSky

💡 TuLender tip: Use it to pay for Netflix or gas. Keep the balance low — under 30% of the limit — and pay it off in full every month.

2. Build a Healthy Mix (Credit Mix = 10%)

Mortgage lenders love seeing:

✅ At least 2 installment loans (like a car loan, student loan, or a credit-builder loan)

✅ At least 3 revolving accounts (credit cards, lines of credit)

✅ All balances below 30% of your limit

❌ No collections, foreclosures, or late payments

If you don’t have student loans or a car payment, no problem. You can use

3. Never Miss a Payment (Payment History = 35%)

Even one late payment can tank your score. Set up auto-pay for the minimum due — even if it’s just $25.

✅ Always on time = healthy score

❌ 30+ days late = major FICO drop

4. Don’t Max Out Your Cards (Amounts Owed = 30%)

Lenders care about how much of your credit limit you’re using.

Example:

If your card limit is $500, don’t let your balance go over $150 (30%).

Want a better boost? Keep it under 10%.

5. Let Your Accounts Age (Length = 15%)

Time matters. The longer you’ve had credit, the better.

Don’t close old accounts, even if you don’t use them much.

Ask a family member with great credit to add you as an authorized user. You get the benefit of their long history.

6. Go Easy on New Applications (New Credit = 10%)

Applying for lots of cards or loans in a short time looks risky.

✅ Space out applications

✅ 1–2 new accounts every 6 months is plenty

❌ Avoid “store cards” unless you really need them

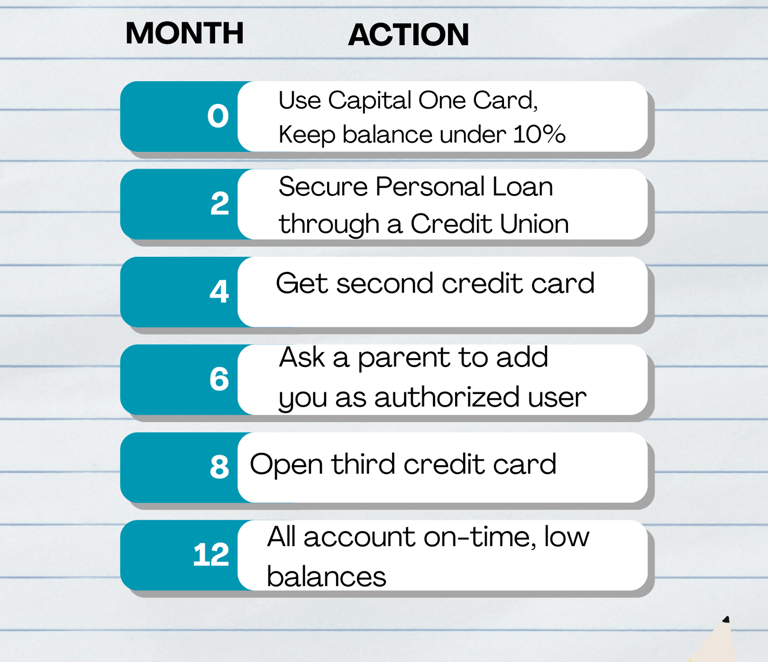

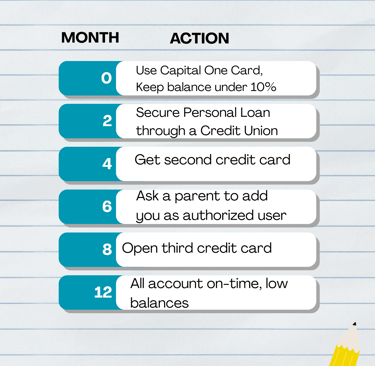

🧠 Real-Life Example: Gen Z Mortgage Score Strategy

Let’s say you’re 22 and just got your first Capital One card. Here’s how you can get mortgage-ready in 12–18 months:

Final Thought: Credit Is a Long Game

You don’t need to be rich or have a ton of debt to build credit. You just need to play it smart, be consistent, and start early. That 3-digit number could be your key to owning your first home before 30.