From Wall Street to Your Street: Bonds Explained for First-Time Homebuyers

As a mortgage advisor, staying on top of the bond market isn't just part of my job—it's essential. Every day, I analyze market movements to guide my clients through some of the most important financial decisions of their lives. Whether it's interest rates, mortgage terms, risk, or principal, understanding the bond market allows me to present clear, informed options tailored to each buyer’s needs.

5/15/20252 min read

What Are Bonds?

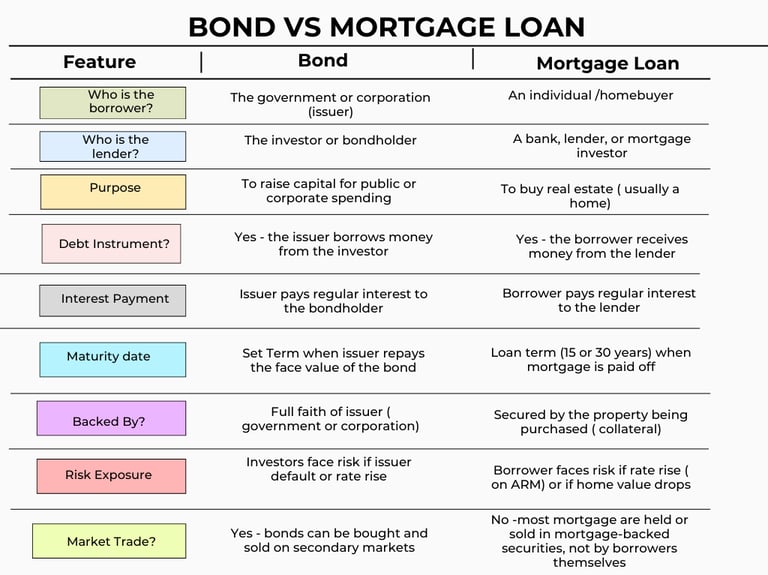

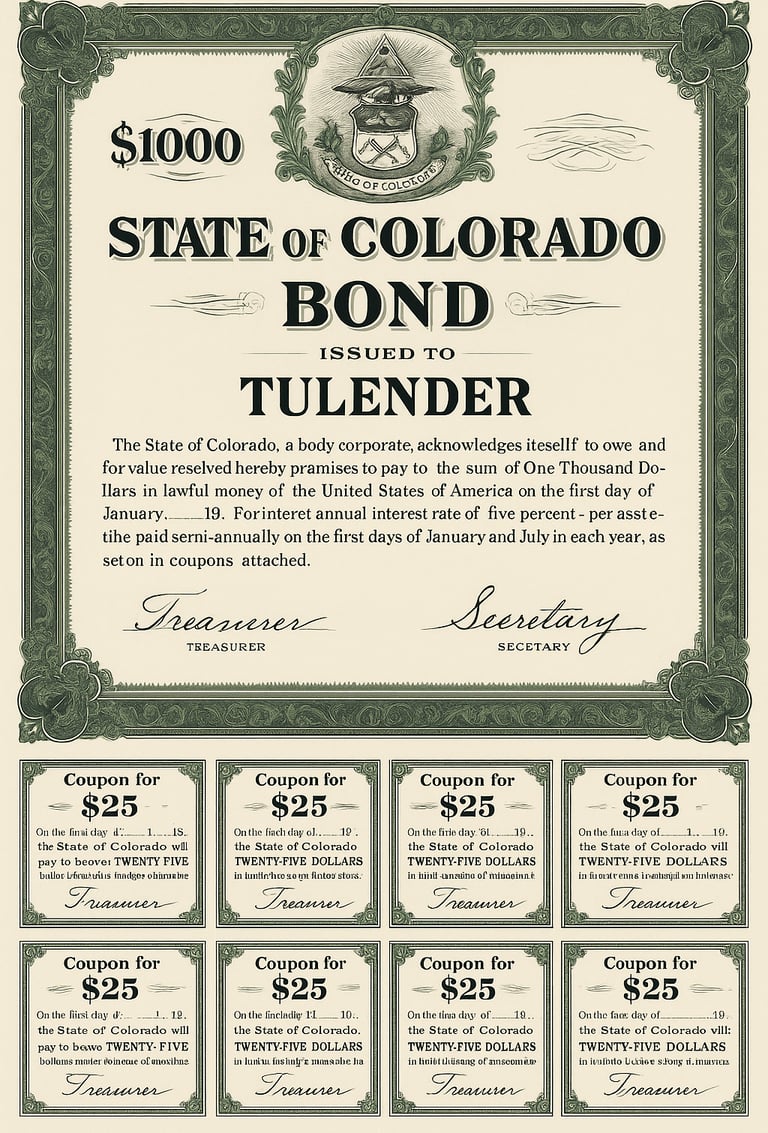

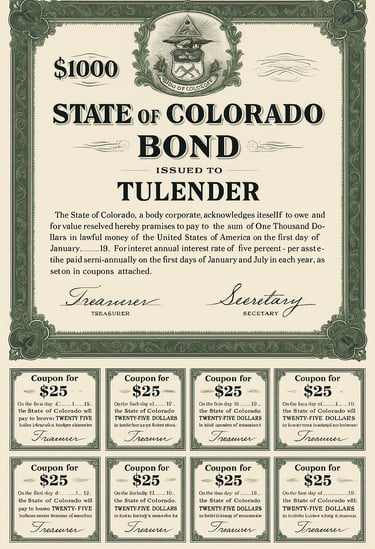

Bonds, also known as Treasury securities, are debt instruments issued by the U.S. Department of the Treasury to fund government spending that isn’t covered by tax revenue.

In simple terms, a bond is an IOU: the U.S. government borrows money from investors and promises to repay it in the future—with interest.

But it's not just the government that issues bonds. Corporations, government agencies, and municipalities also issue bonds to raise capital. These issuers pay investors regular interest (known as coupon payments) and return the principal at the maturity date.

As a mortgage broker, it's important to track the activity of major agencies like Fannie Mae and Freddie Mac, which issue bonds to fund the residential mortgage market. These agency bonds directly influence mortgage rates and market liquidity.

While most people tend to follow the stock market, it's worth noting that the bond market is actually about three times larger than the stock (or equity) market. Despite getting less media attention, the bond market plays a critical role in shaping interest rates, borrowing costs, and overall economic health.

This comparison is especially useful for explaining to clients why bond yields influence mortgage rates—because investors who buy mortgage-backed securities are essentially deciding whether they want to lend money for mortgages or buy Treasuries. The risk and return between the two must align.

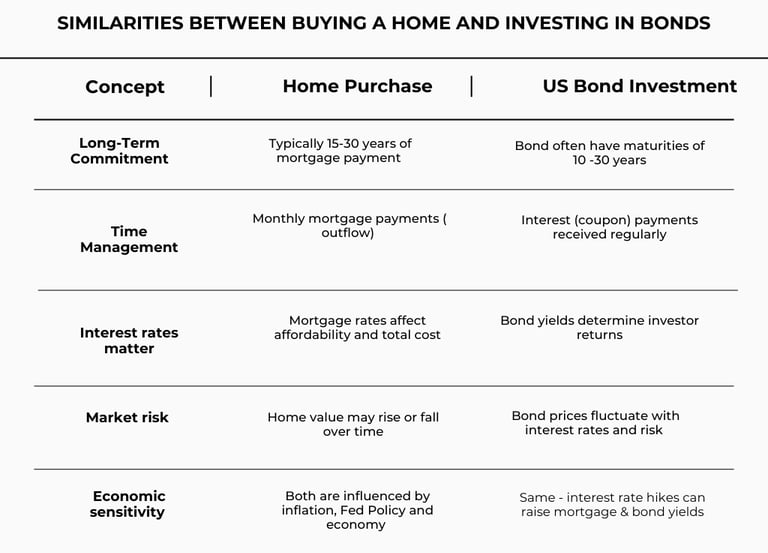

Is Purchasing a Home Like Investing in the U.S. Bond Market?

Short answer: Yes, in some ways — but with key differences.

Let’s break it down:

While investing in the bond market can offer predictable returns and income, buying a home offers something far more meaningful.

Yes, your home is likely to appreciate over time, building equity that can support your retirement, fund your children’s education, or serve as a financial cushion down the road. But beyond the numbers, the greatest return on a home isn’t measured in dollars — it’s measured in memories.

A home is where you’ll share birthdays, holidays, first steps, and late-night conversations. It’s the place where families grow, traditions begin, and life's most precious moments unfold. That’s an investment no market can match.

This is why you need a mortgage advisor for life

Buying a home isn’t just a financial transaction — it’s a life decision. The right advisor helps you navigate rates, risks, and opportunities, but also stands by your side through every milestone that follows.

That’s exactly why here at Tulender — to guide you not just through one loan, but through every chapter of your homeownership journey.

Let’s build your future, together.